{{parent.title}}

{{parent.title}}

Login

Login

Many students know they’ll have to borrow money to help with college expenses, and that’s normal. Borrowing money responsibly and paying it back on time is a part of life for many of us. So, it’s important to understand what it means to take on student loan debt and how to handle it smartly.

The issues arise when people borrow too much money without a plan to repay it. Without understanding, they’ll pay more over time due to interest.

The question is: How much student debt is too much student debt? And how can you avoid getting in too deep?

Defining “too much” student loan debt

Different people have their own ideas of what too much student debt is. Some students and families have very different philosophies and relationships with borrowing — and with money in general. Financial experts can give tips and guidelines. But ultimately, you have to be comfortable with the idea of borrowing.

Average Student Loan Debt in 2024

First, let’s understand who is borrowing and how much. Student loan borrowers, on average, graduate with around $30,000 in student loan debt. That makes about $1.75 trillion in student loan debt, the vast majority of which is from federal student loans. That’s no small chunk of change. But how much student loan debt is too much?

Experts suggest some general rules of thumb to help you avoid borrowing too much.

Rules of thumb for determining when debt becomes excessive

Rule of thumb #1: borrow less than your expected starting salary after college

This expert advice might be easier said than done. But it’s important to consider how much money you might make after graduation and how long it will take to repay student loans. If the total amount borrowed is less than the starting salary of your first year after school, experts say you should be able to repay your student debt within ten years.

Of course, many college students don’t even know what they want to major in when they start school — let alone their starting salary! And we’ve all seen those TikTok videos where influencers ask teens on the street what they think the average American’s salary is. They get answers like, “Hmm…I dunno, maybe $400k.” Sorry to break it to you, but that’s way off.

Even if you’re not sure about your future job, it’s a good idea to research the fields you’re interested in and find out the typical starting salaries. If you already have a career in mind, you should be able to find information on the salaries you can expect after graduation.

You can check out the Bureau of Labor Statistics (BLS) for salary data across various industries. For example, if you look up the salary of teachers, you’ll see a mean annual wage of $70,340. So, according to this rule of thumb, a teacher shouldn’t borrow more than $70,340 or whatever they expect their annual starting salary to be.

Remember that BLS numbers might not accurately reflect the starting salaries for recent graduates.

Rule of thumb #2: loan payments should be less than 10% of your gross income

Another way to avoid taking on too much student debt and ensure affordable payments is to see how much you’ll pay on your student loans each month after graduation.

This is calculated based on how much you borrow, your loan terms, and what interest rate you’ve received. Your monthly payments shouldn’t exceed 10% of your total gross income. With the free online Loan Simulator, you can play around and see what your monthly student loan payments might look like.

Here’s an example:

If you expect to earn an annual gross income of $50,000 during your first year after college, you would want to make sure your monthly student loan payments aren’t more than $5,000 per year ($50,000 x 10%) or $417 monthly.

Assuming a 6% interest rate and that you’ll use the 10-year repayment period, a monthly payment of $417 would equate to a loan balance of about $37,000 in student loan debt at graduation.

Does allocating 10% of your gross income seem like too much for you? Think ahead and keep in mind what other expenses you might have to cover each month, like rent or a car payment.

Remember that this is a general rule of thumb and doesn’t work in all cases. One important exception is federal student loan income-driven repayment plans, which cap student loan payments at five to 20 percent of discretionary income.

So, for many borrowers who are on income-driven repayment, the monthly payment amount will be determined by income and not the student loan debt balance.

Factors to consider with student loan debt totals

Federal vs. Private Student Loans

Not every student loan is the same—and not all student debt is the same either. In general, there are two types of student loans.

First, we have federal student loans, which the federal government funds. You must complete the FAFSA (Free Application for Federal Student Aid) to determine your eligibility.

If you need money for school, you should explore federal student loans first, as they typically offer lower interest rates and more flexible repayment options than private student loans. If you qualify, federal student loans will be incorporated into your financial aid package.

Next, there are private student loans. Private student loans come from banks and other financial organizations and are credit-based. That means that when you (and most likely, a cosigner) apply, the lender checks your credit.

The main difference with private student loans compared to federal loans is private student loans generally have more strict repayment terms. They don’t automatically offer payment deferment, nor are they generally eligible for income-driven repayment options or forgiveness.

Because of these factors, carefully consider the amount of private student loans you borrow along with your total student loan debt, including both types of loans.

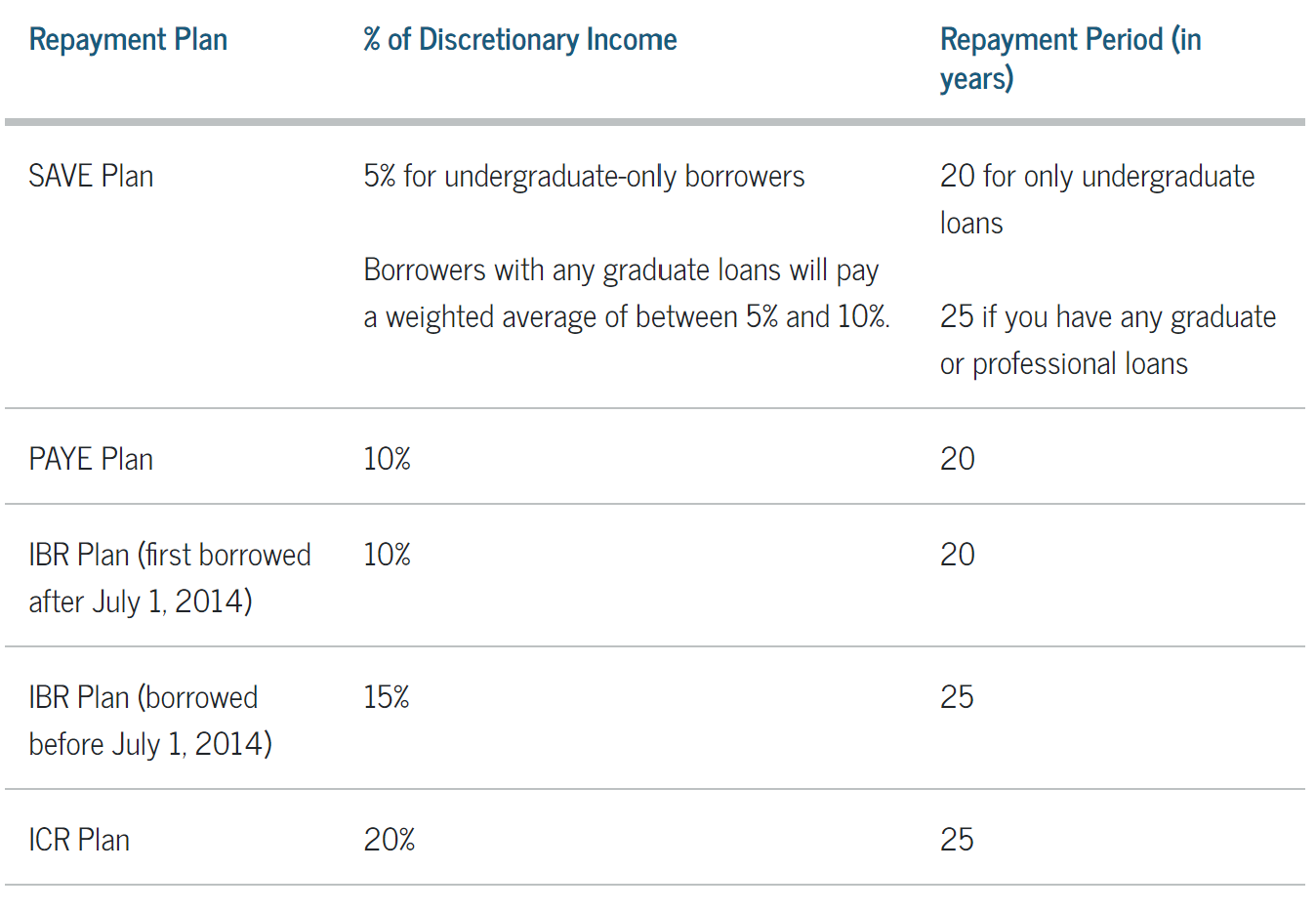

Income-Driven Repayment Plans

Income-driven repayment plans are designed to make student loan payments more manageable for borrowers. The plans base the amount of your monthly loan payment on your discretionary income – that’s the money you have left each month after taxes and paying for necessities like food and housing – rather than how much you borrowed.

If you owe more in student loans than you earn in a year after finishing school, you might have lower monthly payments with this repayment plan.

There are four different income-driven repayment plans. The Dept. of Ed’s Loan Simulator can help you figure out which program might be right for you.

For example, if you have are single, make $50,000 per year after college, and have $50,000 in student loan debt, you may be eligible for an Income-driven repayment plan with initial monthly payments as low as $67 per month.

Federal Student Loan Forgiveness

While plenty of headlines about federal student loan forgiveness and debt relief exist, those programs don’t apply to everyone. And they don’t apply to private student loan debt. But for eligible borrowers, forgiveness can be very valuable.

One common program is Public Service Loan Forgiveness, which many employees of nonprofits and government agencies qualify for. Those who work for qualifying employers as physicians, nurses, or other professionals may qualify for this program to have their student loans forgiven after 10 years of qualifying repayments. This can result in five- to six-figures of student loan debt forgiveness for some borrowers.

Income-driven repayment plans also offer forgiveness over longer periods of time (10 to 25 years of repayment).

The Consequences of Too Much Student Debt

Estimating how much you can afford to borrow for college can be tough. But the last thing you want is to sign paperwork without understanding your future payments—or the long-term consequences. Student loans can impact your finances for many years after graduation, especially if you have too much student loan debt.

Late payments will hurt your credit score

When you don’t make your student loan payments on time, you’re charged a late fee, meaning you must pay more. What’s worse is that repeated late payments negatively impact your credit score.

As an adult, your credit score is really important. You need good credit to get a credit card, car loan, or mortgage. Many property management companies will even do a credit check before renting an apartment to you. Late payments stick with you—and the consequences snowball.

On the upside, making regular, on-time student loan payments can help you positively build your credit.

Risk of Student Loan Default

Defaulting on a student loan means you failed to make the required loan payments. This will affect your credit score and your ability to borrow money in the future. Defaulting on a loan can even lead to wage garnishment, where your employer is legally obligated to withhold a portion of your pay to cover the debt.

According to our research, over one million borrowers default for the first time every year, and first-time defaults typically happen within the first three years.

Generally, not living your best life

Not surprisingly, most Americans with student loan debt are younger, in their twenties and thirties. With student loans hanging over your head, you’ll probably have less money for fun things like nights out with friends, a new car, or traveling. You might even need to delay major life events like buying a home, saving for retirement, getting married, and having children.

Reducing and managing student debt

If you want to avoid taking on too much student loan debt, there are steps you can take to cut the cost of college—and maybe even pay for school without any loans.

Start planning early—however you can

This one’s obvious: if you want to avoid too much debt, it’s worth it to start saving early. And even if you can’t start saving for college right now, you can make a plan for when and how you’ll start saving.

The average 529 balance is about $28,000, and for most families this takes many years of investment to reach.

Open a 529 college savings plan

One popular way to start saving for college is to invest in a 529 plan for yourself, your kids, or your grandkids. A 529 plan is a tax-advantaged account that enables you to save money and use the funds that grow over time for college expenses or another form of higher education. This money grows and can be withdrawn tax-free, which is a big advantage compared to other savings accounts.

Apply for as many scholarships as you can

Scholarships are free money for college you don’t need to pay back—and they’re not just for straight-A students and all-star athletes anymore. There are scholarships for almost every hobby and interest. There are scholarships for whatever you’re into, from crafting to gaming to volunteering.

And keep your eyes open for local scholarships, too—they tend to get fewer applicants and can be less competitive. Ask your school counselor about local scholarship opportunities. And parents, find out if your employer has scholarship opportunities for employees’ children. A lot of companies award scholarships every year for just that purpose.

Sure, these scholarships won’t always cover the entire cost of college. But even a few thousand dollars can cover books, transportation, and a laptop.

Go to a public college or university

Public colleges and universities—especially those in your home state—will be less expensive than private schools. According to The College Board, these are the 2023-2024 average tuition and fees for full-time undergraduate students for one academic year:

Public four-year in-state: $11,260

Private non-profit four-year: $41,540

Choosing a public college or starting at a community college can potentially limit the amount of student loans you need to borrow.

Find part-time work or an internship

Working a part-time job while in high school is a great way to save money for college. You might also qualify fo work-study: a part-time job through your college that can help you pay for school. The Federal Work-Study program is a form of financial aid. The only way to determine if you qualify is by filling out the FAFSA.

Many college students also pursue internships. These are a great way to earn money for school, gain valuable work experience, and maybe even make some connections that can be helpful when it’s time to find a full-time job.

Making Smart Decisions

Choosing to take out student loans for college—and how much you take out—is a big decision. But with a little research, a solid plan, and some cost-cutting measures, you can make a responsible choice you feel good about.

Frequently Asked Questions (FAQs)

What is considered a lot of student loan debt?

A lot of student loan debt is more than you can afford to repay after graduation. For many, this means having more than $70,000 – $100,000 in total student debt.

Is $100,000 in student loans too much?

It’s hard to say what’s too much for everyone, broadly speaking. However, borrowing $100,000 or more is considered to be a lot and isn’t normal for the average student. Most jobs don’t pay over $100,000 right out of school, so it could be a struggle to have that much student loan debt.